A seasoned colleague recently told me that some PowerPoint presentations have no power and make no point.

But sometimes, a picture really is worth a thousand words. Or maybe — in the case of any meaningful discussion of health reform, thanks to its density and complexity — it might be worth 10,000 words. Hence our handy little exhibit.

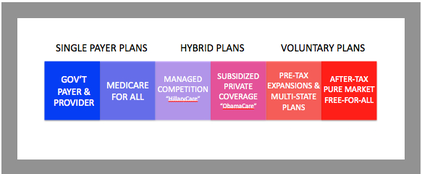

This picture captures the 10,000 words it would require to explain with technical precision where President Obama’s Affordable Care Act fits relative to all health reform plans. It places “ObamaCare” along an ideologically scaled continuum of all serious reform options developed, debated and discarded or ignored since the 1980s.

They are all here: from the single-payer, centrally controlled models popular with those who detest corporations and the influence of money in medicine — two actual, not imagined “government takeovers of health care” — to two free market, laissez-faire models favored by those who detest regulation and the heavy hand of government in medicine.

On the far left, the federal (or provincial) government is the main insurer, owns most hospitals, and employs most doctors. This pure form of single payer seems to be supported or reviled in equal measure — especially by the nation’s physicians. As a model for nationwide reform, it is like religion — people either believe it will be health care’s Messiah, or the anti-Christ, and no one will convince them otherwise. This model is the foundation for many of the systems in Europe, and the systems in Canada, Australia, New Zealand, and Singapore. Unbeknownst to many in their care, there are actually two working systems based on this model in the U.S. today: Kaiser and the Veterans Health Administration.

The second model, Medicare-for-All, differs from the pure form of single payer by retaining the current independence of most hospitals and doctors. This model jettisons private insurance companies, while an all-encompassing Medicare program pays for covered care delivered by today’s crazy quilt of providers: large and small groups, for-profit, religious-affiliated, independent, academic, the works. This is what Medicare beneficiaries have today — except for the 27 percent who opt for Medicare Advantage plans offered by private insurers. It is supported by those who believe it would bring the relative efficiencies, fairness and low administrative costs of Medicare to all, and reviled by those who think Medicare works like hell. Because there are oceans of data to support both views, this too is ultimately a matter of secular faith: government, good; government, evil.

Next is “managed competition,” the basis for the plan proposed by President and Hillary Clinton. This model is built on the current system of multiple private insurers and providers, but highly organizes and regulates both, mandating employers and individuals to participate and requiring everyone, with or without current coverage, to give up what they have and commit to one of several competing vertical insurer/provider entities. This model is based on managed care theories developed in the ’70s and ’80s, and when proposed by the Clintons in the early ’90s, was popular with much of the Washington technocracy and vilified by conservatives.

Most Republicans and health industry critics attacked “Hillarycare” as cumbersome, over-engineered, and hyper-bureaucratic. It was destroyed in the court of public opinion by an insurer-funded TV ad campaign — “Harry & Louise” — that people remember better than any details of the plan itself. Modified versions of this model exist in Germany and Israel, and in a handful of U.S. markets (e.g., San Francisco and Portland, Oregon, sort of) with vertically integrated providers who compete with Kaiser.

To the right of “Hillarycare” is President Obama’s Patient Protection and Affordable Care Act, known as “PPACA, “the ACA,” or “Obamacare.” It retains most of the features of the current employer, insurance and provider systems, but expands all of its current dimensions by mandating that most of the uninsured participate in it, unless their incomes are low enough to qualify them for an expanded version of Medicaid.

Obamacare requires insurers to compete for customers through health insurance exchanges, deeply misunderstood and thus easily politicized creatures, as I discussed here last week. Obamacare outlaws insurers’ discrimination — and price-discrimination — against people with prior health problems. And it standardizes insurance coverage by market to focus insurer competition on price and service rather than plan design. Because Obamacare requires insurers to cover all comers — and does away with caps on those with catastrophically expensive medical situations — it is funded by mandated participation by almost everyone, either directly or through employers. It is based on principles of market competition developed by conservatives and proposed by Republicans as an alternative to Hillarycare.

To the right of Obamacare are two versions of free market models — containers for the “replacement” options crafted by or pointed to those who want to “repeal and replace” Obamacare. Both shift all purchasing decisions about coverage and plan design to individuals and insurers, believing this will reshape markets and drive efficiency in pricing and overall medical resource use. Most versions do not require anyone to purchase insurance, nor any insurer to cover anyone.

The two models differ mainly with regard to how health insurance and non-covered medical expenses are treated by the tax code. Proponents of the model on the far right believe that market distortions created by the tax deductibility of health insurance and expenses are enormous, and the extra political mile it would take to eliminate these well worth the effort in terms of marketplace correction and health system self-reform.

The first of the two models on the right actually expands the current system of tax deductibility of health insurance and direct medical expenses to individuals and the self-employed. Its architects believe this would level the playing field for insurance purchasing, ease out the distorting role of the employer from the system, and convert much of what is covered today by health insurance to health savings accounts and cash payment. The model would allow small businesses and individuals to pool together to buy whatever coverage they wanted across state-lines — the “Association Health Plans” often put forward by Republicans — a modified version of which is included in Obamacare as the “Multi-State Plans.” We have a version of this model in the US right now in miniature: dentistry.

The model on the far right also seeks to reduce the role of the employer in health care, but is structured on the belief that a better, faster way to get there is by removing the tax deductibility health care spending. Its proponents believe this would extract employers from the system in short order, convert health insurance into something resembling auto and homeowners insurance, and maximize the power of market forces to control health care spending in general. Under this model, everyone is free to purchase whatever mix of insurance and services they want and can find, from whatever organization will sell it to them, at whatever price the market yields. Modified versions of this model exist in China and India on top of threadbare single-payer systems incapable of serving the needs of their large and growing populations and emerging middle classes.

The proponents of both models on the right believe their inherent pricing efficiency would drive the marketplace to very high deductible insurance plans while converting routine medical care to a cash-and-carry system. Both models would subsidize the uninsured and others priced out of these markets with either a “premium support” or “voucher” program — two ideas that sound similar but play out very differently as health care costs increase.

The core economic reform mechanisms of the two models on the right show up every few years by newcomers to health care from the business sector, usually after a jarring personal encounter with the health care system. The latest entry is David Goldhill and his Catastrophic Care: How American Health Care Killed My Father — and How We Can Fix It. The subsidy mechanism — loaded with dangerous ammo for semantic and political branding wars over “premium support” vs. “voucher” — is the economic fulcrum in Congressman Paul Ryan’s proposal for reforming Medicare.

The above illustration of health reform plans along a political continuum reveals one of the more bitter political ironies of our time: President Obama’s health care reform law is based, for the most part, on right-of-center ideas.

This may have escaped the notice of most journalists and pundits and, for obvious reasons, the president’s legion of political opponents. But it is an odd and awkward fact for those in the trenches of health policy who care more about reforming the health care system — if only in hard-fought, belated baby steps — than they do about the purity of models, the promotion of a broader ideology, or the mud-slinging and name-calling that has come to define our national politics.

That Obamacare is a right-of-center plan, especially when viewed relative to all viable alternatives, explains why it has so little political support from either side. Liberals hate Obamacare because it is not single-payer, and feeds tens of millions of newly insured people to what they revile as a money-gobbling, profit-obsessed health insurance dragon. Conservatives hate Obamacare because it is the heavy, stupid hand of Big Government choking whatever air is left out of the current, dysfunctional health insurance market. That, or because they cannot see beyond their political rage at President Obama to recognize their own ideas at the core of his health reform plan.

Ideologically, this makes Obamacare a political orphan. And Washington, D.C., even back in the days of decorum and actual policy discussions, has never been kind to political orphans. How else to explain why the president (e.g., in his inaugural address, State of the Union speech) makes almost no mention of what could prove to be his signature domestic achievement — even as tens of thousands of Americans working for health insurers, hospitals, physician practices and other health care organizations grind away at its implementation.

Perhaps this is because Obamacare, which will affect to some unknown degree nearly one-sixth of the U.S. economy, has been reduced to a broken political piñata. Another seasoned colleague recently told me that the reason I do not understand the disconnect here is because the health reform “debate” has nothing to do with the substance of Obamacare as policy and everything to do with its politics.

Those interested in understanding where the plan fits into decades of earnest struggle with this difficult and important subject — rather than scoring political points against the president — would be well advised to consult this one PowerPoint slide.

But sometimes, a picture really is worth a thousand words. Or maybe — in the case of any meaningful discussion of health reform, thanks to its density and complexity — it might be worth 10,000 words. Hence our handy little exhibit.

This picture captures the 10,000 words it would require to explain with technical precision where President Obama’s Affordable Care Act fits relative to all health reform plans. It places “ObamaCare” along an ideologically scaled continuum of all serious reform options developed, debated and discarded or ignored since the 1980s.

They are all here: from the single-payer, centrally controlled models popular with those who detest corporations and the influence of money in medicine — two actual, not imagined “government takeovers of health care” — to two free market, laissez-faire models favored by those who detest regulation and the heavy hand of government in medicine.

On the far left, the federal (or provincial) government is the main insurer, owns most hospitals, and employs most doctors. This pure form of single payer seems to be supported or reviled in equal measure — especially by the nation’s physicians. As a model for nationwide reform, it is like religion — people either believe it will be health care’s Messiah, or the anti-Christ, and no one will convince them otherwise. This model is the foundation for many of the systems in Europe, and the systems in Canada, Australia, New Zealand, and Singapore. Unbeknownst to many in their care, there are actually two working systems based on this model in the U.S. today: Kaiser and the Veterans Health Administration.

The second model, Medicare-for-All, differs from the pure form of single payer by retaining the current independence of most hospitals and doctors. This model jettisons private insurance companies, while an all-encompassing Medicare program pays for covered care delivered by today’s crazy quilt of providers: large and small groups, for-profit, religious-affiliated, independent, academic, the works. This is what Medicare beneficiaries have today — except for the 27 percent who opt for Medicare Advantage plans offered by private insurers. It is supported by those who believe it would bring the relative efficiencies, fairness and low administrative costs of Medicare to all, and reviled by those who think Medicare works like hell. Because there are oceans of data to support both views, this too is ultimately a matter of secular faith: government, good; government, evil.

Next is “managed competition,” the basis for the plan proposed by President and Hillary Clinton. This model is built on the current system of multiple private insurers and providers, but highly organizes and regulates both, mandating employers and individuals to participate and requiring everyone, with or without current coverage, to give up what they have and commit to one of several competing vertical insurer/provider entities. This model is based on managed care theories developed in the ’70s and ’80s, and when proposed by the Clintons in the early ’90s, was popular with much of the Washington technocracy and vilified by conservatives.

Most Republicans and health industry critics attacked “Hillarycare” as cumbersome, over-engineered, and hyper-bureaucratic. It was destroyed in the court of public opinion by an insurer-funded TV ad campaign — “Harry & Louise” — that people remember better than any details of the plan itself. Modified versions of this model exist in Germany and Israel, and in a handful of U.S. markets (e.g., San Francisco and Portland, Oregon, sort of) with vertically integrated providers who compete with Kaiser.

To the right of “Hillarycare” is President Obama’s Patient Protection and Affordable Care Act, known as “PPACA, “the ACA,” or “Obamacare.” It retains most of the features of the current employer, insurance and provider systems, but expands all of its current dimensions by mandating that most of the uninsured participate in it, unless their incomes are low enough to qualify them for an expanded version of Medicaid.

Obamacare requires insurers to compete for customers through health insurance exchanges, deeply misunderstood and thus easily politicized creatures, as I discussed here last week. Obamacare outlaws insurers’ discrimination — and price-discrimination — against people with prior health problems. And it standardizes insurance coverage by market to focus insurer competition on price and service rather than plan design. Because Obamacare requires insurers to cover all comers — and does away with caps on those with catastrophically expensive medical situations — it is funded by mandated participation by almost everyone, either directly or through employers. It is based on principles of market competition developed by conservatives and proposed by Republicans as an alternative to Hillarycare.

To the right of Obamacare are two versions of free market models — containers for the “replacement” options crafted by or pointed to those who want to “repeal and replace” Obamacare. Both shift all purchasing decisions about coverage and plan design to individuals and insurers, believing this will reshape markets and drive efficiency in pricing and overall medical resource use. Most versions do not require anyone to purchase insurance, nor any insurer to cover anyone.

The two models differ mainly with regard to how health insurance and non-covered medical expenses are treated by the tax code. Proponents of the model on the far right believe that market distortions created by the tax deductibility of health insurance and expenses are enormous, and the extra political mile it would take to eliminate these well worth the effort in terms of marketplace correction and health system self-reform.

The first of the two models on the right actually expands the current system of tax deductibility of health insurance and direct medical expenses to individuals and the self-employed. Its architects believe this would level the playing field for insurance purchasing, ease out the distorting role of the employer from the system, and convert much of what is covered today by health insurance to health savings accounts and cash payment. The model would allow small businesses and individuals to pool together to buy whatever coverage they wanted across state-lines — the “Association Health Plans” often put forward by Republicans — a modified version of which is included in Obamacare as the “Multi-State Plans.” We have a version of this model in the US right now in miniature: dentistry.

The model on the far right also seeks to reduce the role of the employer in health care, but is structured on the belief that a better, faster way to get there is by removing the tax deductibility health care spending. Its proponents believe this would extract employers from the system in short order, convert health insurance into something resembling auto and homeowners insurance, and maximize the power of market forces to control health care spending in general. Under this model, everyone is free to purchase whatever mix of insurance and services they want and can find, from whatever organization will sell it to them, at whatever price the market yields. Modified versions of this model exist in China and India on top of threadbare single-payer systems incapable of serving the needs of their large and growing populations and emerging middle classes.

The proponents of both models on the right believe their inherent pricing efficiency would drive the marketplace to very high deductible insurance plans while converting routine medical care to a cash-and-carry system. Both models would subsidize the uninsured and others priced out of these markets with either a “premium support” or “voucher” program — two ideas that sound similar but play out very differently as health care costs increase.

The core economic reform mechanisms of the two models on the right show up every few years by newcomers to health care from the business sector, usually after a jarring personal encounter with the health care system. The latest entry is David Goldhill and his Catastrophic Care: How American Health Care Killed My Father — and How We Can Fix It. The subsidy mechanism — loaded with dangerous ammo for semantic and political branding wars over “premium support” vs. “voucher” — is the economic fulcrum in Congressman Paul Ryan’s proposal for reforming Medicare.

The above illustration of health reform plans along a political continuum reveals one of the more bitter political ironies of our time: President Obama’s health care reform law is based, for the most part, on right-of-center ideas.

This may have escaped the notice of most journalists and pundits and, for obvious reasons, the president’s legion of political opponents. But it is an odd and awkward fact for those in the trenches of health policy who care more about reforming the health care system — if only in hard-fought, belated baby steps — than they do about the purity of models, the promotion of a broader ideology, or the mud-slinging and name-calling that has come to define our national politics.

That Obamacare is a right-of-center plan, especially when viewed relative to all viable alternatives, explains why it has so little political support from either side. Liberals hate Obamacare because it is not single-payer, and feeds tens of millions of newly insured people to what they revile as a money-gobbling, profit-obsessed health insurance dragon. Conservatives hate Obamacare because it is the heavy, stupid hand of Big Government choking whatever air is left out of the current, dysfunctional health insurance market. That, or because they cannot see beyond their political rage at President Obama to recognize their own ideas at the core of his health reform plan.

Ideologically, this makes Obamacare a political orphan. And Washington, D.C., even back in the days of decorum and actual policy discussions, has never been kind to political orphans. How else to explain why the president (e.g., in his inaugural address, State of the Union speech) makes almost no mention of what could prove to be his signature domestic achievement — even as tens of thousands of Americans working for health insurers, hospitals, physician practices and other health care organizations grind away at its implementation.

Perhaps this is because Obamacare, which will affect to some unknown degree nearly one-sixth of the U.S. economy, has been reduced to a broken political piñata. Another seasoned colleague recently told me that the reason I do not understand the disconnect here is because the health reform “debate” has nothing to do with the substance of Obamacare as policy and everything to do with its politics.

Those interested in understanding where the plan fits into decades of earnest struggle with this difficult and important subject — rather than scoring political points against the president — would be well advised to consult this one PowerPoint slide.

RSS Feed

RSS Feed